Tax Reconciliation

A numerical reconciliation of tax expense to accounting profit is required under IAS 12. This article walks through the concept, the difference between permanent and temporary differences, and how deferred tax fits into the reconciliation.

Xian Hui

2 December 2025

Quick answer

What is a tax reconciliation and why is it required under IAS 12?

A tax reconciliation under IAS 12 explains how total income tax expense relates to accounting profit. It highlights items such as non-taxable revenue, non-deductible expenses, tax losses, and foreign tax rate differences. The reconciliation includes both current and deferred tax, so permanent differences appear as reconciling items while temporary differences do not, because deferred tax already accounts for timing differences.

Tax Reconciliation

A numerical reconciliation of tax expense to accounting profit multiplied by the applicable tax rate is required under paragraph 81(g) of IAS 12 Income Taxes (equivalent to SFRS 12). Entities may also present a reconciliation between the average effective tax rate and the applicable tax rate, but reconciling tax expense is more direct and therefore more common in practice.

SFRS for Small Entities does not require this disclosure.

Luca does not compute income tax. It does not calculate current or deferred tax. Because of that, Luca cannot auto-populate the tax reconciliation. Still, here is a common way this reconciliation is prepared in practice.

What is Income Tax?

The tax expense referred to in IAS 12.81(g) is not the same as the final tax payable shown in a tax computation or Form C or C-S in Singapore.

Income tax expense is the total tax recognised in profit or loss for the period. It usually includes:

- Current tax for the year

- Adjustments to prior years' current tax, such as under- or over-provision

- Deferred tax, arising from temporary differences

This total is the ending figure that the numerical reconciliation must explain.

What is the Purpose of Tax Reconciliation?

IAS 12.84 explains that the purpose of the tax reconciliation is to help users of financial statements understand whether the relationship between tax expense and accounting profit (i.e. profit before tax) is unusual, and to highlight significant factors that may influence this relationship in future periods.

These factors may include:

- Revenue or expenses that are not taxable

- Tax losses

- Different tax rates in foreign jurisdictions

In Singapore, normal trading companies prepare tax computations starting with profit before tax. IRAS administers corporate income tax, and the standard corporate tax rate is 17%. This makes the reconciliation process easier. Over time, when working papers are carried forward over many years, it can create the impression that the tax reconciliation is the same as the tax computation. They are not. The tax computation determines the tax payable. The tax reconciliation explains how the total tax expense relates to accounting profit.

For some entities, such as investment companies, the tax computation does not start with profit before tax. The same disclosure requirement under IAS 12 still applies. The format of the tax computation does not change how the tax reconciliation is presented.

Why do permanent differences appear in the reconciliation but temporary differences do not?

Because the reconciliation explains the total tax expense, which already includes deferred tax, the items described above as revenue or expenses that are not taxable should be understood as relating only to permanent differences — items that are never taxable or never deductible. Only permanent differences will appear in the tax reconciliation.

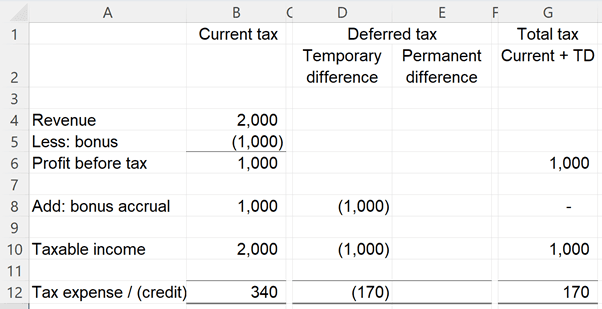

If an expense is added back in the current tax computation — for example, a bonus accrual in Singapore, where the deduction is allowed only when paid — this is a temporary difference. The add-back increases current taxable income, but at the same time you recognise a deferred tax asset with a deferred tax credit in profit or loss.

The table above illustrates this. The deferred tax credit offsets the current tax expense arising from the temporary difference. At the total level, temporary differences do not create reconciling items in the tax reconciliation.

Viewed from another angle, IAS 12 requires income taxes to be recognised in profit or loss in the same period the related income is recognised. This is the matching principle, and deferred tax ensures this alignment.

How does the balance sheet approach work compared to the profit and loss approach?

The example above uses the profit and loss approach to compute temporary differences and the resulting deferred tax impact. This method is simple, but it has a key weakness. When the bonus is paid in the following year and the tax deduction is finally allowed, the entry may be recorded directly against the accrual (Dr Bonus Accrual; Cr Cash). Because it does not pass through profit or loss, the related tax adjustment may be missed.

IAS 12 adopts a balance sheet approach. It requires deferred tax to be assessed by comparing the accounting carrying amount and the tax base of each asset and liability. This method is more complete because it captures all differences through the balance sheet. Its disadvantage is that it is less intuitive. The offsetting effect between current tax and deferred tax is not always obvious.

In practice, many accountants prepare both and compare the results. The movement in deferred tax assets or liabilities under the balance sheet method should match the deferred tax expense or credit derived from the profit and loss method.

Most accountants recognise deferred tax in the books using the balance sheet approach but prepare the tax reconciliation using the profit and loss approach because it is easier to explain. So, when the two do not match, the tax reconciliation will show an unreconciled difference.

If the difference is small, it is often grouped under "other" or included within the line with the largest amount. However, a small net difference may hide two offsetting errors. It is good practice to investigate all differences.

Once the concept is clear, identifying the source of any difference becomes much easier.

What are common reconciling items in a Singapore tax computation?

In a Singapore tax computation, the following adjustments are common:

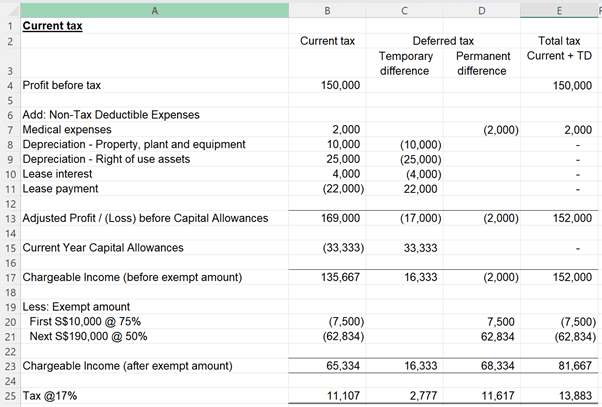

Medical expenses: These are capped at 1% of total employee remuneration. Any amount above the cap is never deductible, whether in the current year or in future years. This is a permanent difference.

Depreciation of property, plant and equipment (PPE) and capital allowance: Accounting depreciation is added back, but the tax laws allow the qualifying cost to be deducted as capital allowance. Both relate to the same asset, so the net difference is usually a temporary difference arising from timing.

Depreciation of right-of-use (ROU) assets, lease interest, and lease payments: For tax purposes, leases are classified as either operating leases or financing leases. If the lease is treated as an operating lease, the ROU asset is not regarded as PPE and the lease liability is not treated as a borrowing. As a result, the ROU depreciation and lease interest are added back in the tax computation. The lease payments are deductible when paid. Since the total lease cost will eventually be reflected in both profit or loss and the tax computation, the net differences here are temporary differences.

Note that PPE depreciation and ROU depreciation are not always temporary differences. If an asset does not qualify for any tax deduction at all, the accounting depreciation becomes a permanent difference. Examples include private cars, owned buildings, renovation costs above SGD 300,000 within 3 years, or assets not used in a trade.

The table above separates the tax adjustments into temporary and permanent differences.

Except for medical expenses and the exempt amount, all other tax adjustments here are temporary differences.

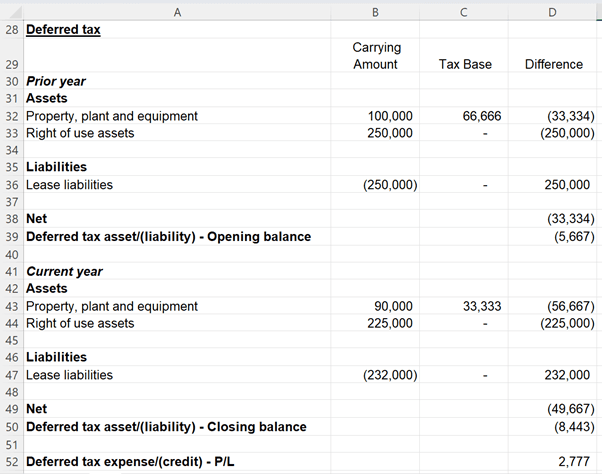

The deferred tax computation below applies the balance sheet approach. Each item is compared by carrying amount and tax base to determine the temporary difference.

It is not a coincidence that the deferred tax expense from the balance sheet approach matches the amount from the temporary difference column in the profit and loss approach. They are meant to agree.

When the two do not match, one effective way to investigate is to compare the movements between opening and closing balances for each asset or liability with the temporary differences identified in the profit and loss approach.

For example:

- PPE carrying amount moved from $100,000 to $90,000 — a decrease of $10,000. This matches the depreciation that was added back in the tax computation.

- PPE tax base moved from $66,666 to $33,333 — a decrease of $33,333. This matches the capital allowance claimed.

These cross-checks help confirm that the deferred tax movements have been captured correctly.

What does a tax reconciliation look like in practice?

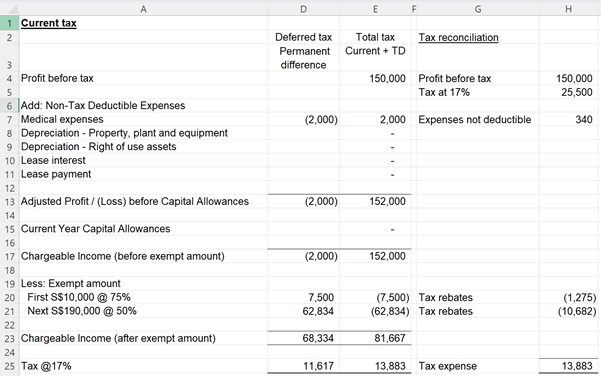

Now that the deferred tax amounts from both the balance sheet approach and the profit and loss approach are aligned, we can prepare the tax reconciliation.

Only the tax effect of permanent differences (using 17% or the applicable rate) will appear as reconciling items. In the table below, one column reflects the amounts after taking into account the offsetting impact of temporary differences. In other words, it shows the permanent differences.

The standards do not prescribe a fixed format for the tax reconciliation. The disclosure must simply help users understand the relationship between tax expense and accounting profit.

Common categories include:

- Revenue that is exempt from tax

- Expenses that are not deductible

- The effect of tax losses

- Differences in foreign tax rates

It is also common to see reconciling items arising from unrecognised deferred tax assets. Entities sometimes do not recognise deferred tax assets if future utilisation of the tax credits is not probable. In such cases, the unrecognised amount is presented as a reconciling item (deferred tax asset or tax credits not recognised). When the tax credits are later utilised, the utilisation is also shown as a reconciling item (utilisation of previously unrecognised tax credits).

Deferred tax liabilities, however, should generally be recognised unless the amount is immaterial. If an immaterial deferred tax liability is not recognised, the impact is often grouped under "other".

Luca provides suggested categories commonly seen in financial statements, which appear in the disclosure screen of the financial statement generation workflow.

Current Tax

While this article focuses more on deferred tax, current tax remains an important part of the total tax expense. It is usually more straightforward, but certain components can still affect the tax reconciliation.

A common example is adjustments to prior year current tax. These true-up adjustments arise when the income tax filing for the previous year of assessment is finalised, and they appear as reconciling items in the tax reconciliation.

Frequently asked questions

This information has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax, or other professional advice.

Related articles

library

Should ACRA Raise the Audit Threshold?

ACRA is reviewing audit exemption thresholds for Singapore companies. This article argues that the real question is not about size thresholds but about who should decide whether an audit is necessary — and why the answer should be shareholders.

library

Expense Presentation by Nature or by Function

Under IFRS, expenses in the income statement can be presented by nature or by function. This choice affects comparability, disclosure requirements, and the quality of information available to users.

library

How to Build a Chart of Accounts that Drives Value

A well-structured chart of accounts is more than a list of account names. This article explains how to design a COA with an output-driven mindset, use numbering conventions effectively, and avoid common pitfalls.