Expense Presentation by Nature or by Function

Under IFRS, expenses in the income statement can be presented by nature or by function. This choice affects comparability, disclosure requirements, and the quality of information available to users.

Xian Hui

8 March 2026

Quick answer

What is the difference between presenting expenses by nature and by function under IFRS?

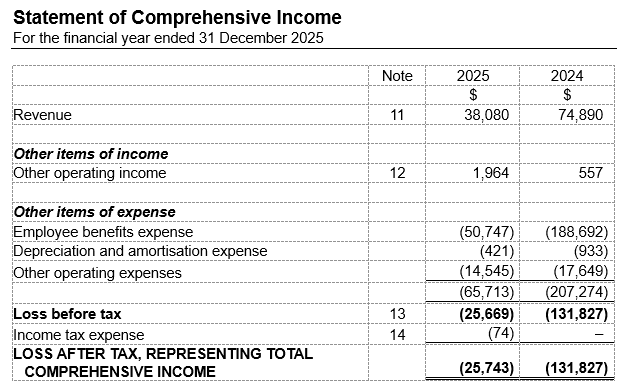

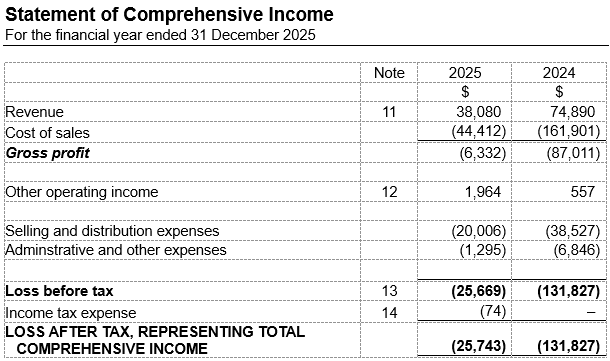

Presenting expenses by nature groups them by type (staff costs, depreciation, etc.), requiring minimal transformation from the chart of accounts. Presenting by function groups them by business role (cost of sales, admin, etc.), which requires allocation and additional disclosure requirements.

Expense Presentation by Nature or by Function

Under International Financial Reporting Standards (IFRS) or its equivalent accounting frameworks (including Singapore Financial Reporting Standards), expenses in the income statement can be presented either by nature or by function. This is a key consideration when preparing financial statements.

IAS 1 Presentation of Financial Statements addresses this choice:

Paragraph 99: An entity shall present an analysis of expenses recognised in profit or loss using a classification based on either their nature or their function within the entity, whichever provides information that is reliable and more relevant.

This choice is not cosmetic. It affects comparability, and the quality of information available to users. Understanding this distinction is also important during financial statements preparation.

The table below summarises the key differences between the two methods.

| Aspect | Analysis by Nature of Expense | Analysis by Function of Expense (Cost of Sales Method) |

|---|---|---|

| Basis of classification | Expenses are classified according to their nature or type (for example employee benefits, depreciation, raw materials) | Expenses are classified according to their function within the entity (for example cost of sales, administrative expenses, distribution costs) |

| Relationship to chart of accounts | Usually aligns directly with natural expense accounts in the ledger | Requires mapping or allocation of natural expenses to functional categories |

| Presentation of gross profit | Gross profit not presented, as expenses are not separated into cost of sales | Gross profit presented, as cost of sales is shown separately |

| Additional disclosures | No additional functional disclosure required | Entities must disclose information about the nature of expenses such as depreciation and employee benefits (IAS 1.104) |

| Typical application | Often used by smaller entities or service-based businesses | Common among manufacturing, trading, and larger entities |

| Judgement in classification | Limited judgement because expenses follow their natural classification | Greater judgement required because expenses must be assigned to functions, and the functional classification of some costs may be ambiguous |

| Allocation of shared costs | Rarely required | Frequently required. Shared costs may need to be allocated across functions, which introduces estimation and judgement |

| Analytical usefulness | Shows expense composition only, with limited insight into operational performance | Adds a functional dimension, enabling analysis of gross margin and operating performance |

What does presenting expenses by nature mean?

This is the most straightforward method. Expenses are grouped according to their type, for example staff costs, depreciation, professional fees, etc.

In practice, most charts of accounts are already structured by nature. Presenting profit or loss by nature therefore requires minimal transformation. It is largely a grouping exercise.

IFRS does not prescribe specific line items. Classification often depends on the entity's operations, industry practice and materiality.

From our observations, this method is common among smaller entities and service-based businesses.

What does presenting expenses by function mean?

Presentation by function groups expenses according to their role within the business. Typical functions include cost of sales, selling and distribution, and administrative expenses.

It is worth noting that entities presenting expenses by function must disclose additional information about the nature of those expenses in the notes. Further discussion will follow.

Entities that present cost of sales will also present gross margin. This format is therefore popular among companies dealing in goods.

However, functional classification is not always straightforward.

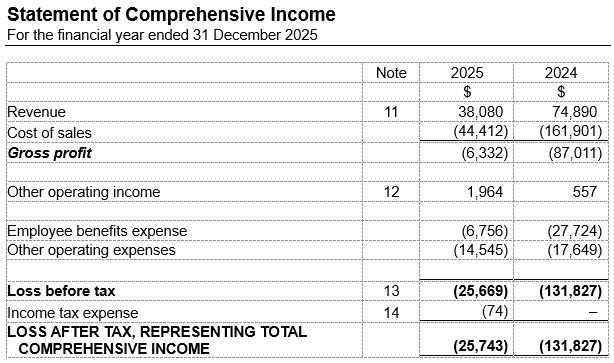

The Allocation Problem in Practice

Most charts of accounts are not designed around functions. Modern systems often introduce an additional reporting dimension to capture functional information. For example, SAP uses a "functional area" dimension.

Designing a chart of accounts by function is rarely practical. To satisfy both functional presentation in the income statement and disclosure of expenses by nature in the notes, the chart of accounts would need to split by function and then by nature. This creates a large and operationally difficult structure.

Among SMEs that present profit or loss by function, many rely on simple grouping without robust allocation. This can create risk.

Expenses such as lease-related expenses, depreciation and staff costs often relate to multiple functions. For example:

- A rented premise used as both showroom and back office

- Founders who handle sales, operations, and administration

If these costs are fully classified as administrative expenses, administrative costs appear high while selling costs appear artificially efficient. Users may draw the wrong conclusions.

The standards do not prescribe detailed allocation methods, but poor allocation reduces information quality.

Additional Disclosure Requirement

Under IAS 1.104, entities presenting expenses by function must disclose additional information about the nature of expenses in the notes. Entities presenting by nature are not required to provide a functional breakdown.

Functional presentation therefore provides an additional analytical dimension.

For larger and more complex entities, this can enhance transparency. Shareholders in such companies are typically not involved in daily operations and rely heavily on financial reporting.

For closely held smaller entities, additional breakdown may provide limited incremental value because owners often have direct operational insight.

Can an entity mix both presentation methods?

In practice, it is common to see a mix. For example:

- Cost of sales and gross margin presented by function

- Staff costs and depreciation presented separately by nature

Based on our reading of IAS 1.99, we think this suggests that an entity should present expenses entirely either by nature or by function. However, we also note that some financial statement preparers interpret IAS 1.99 as allowing a mixture. There were discussions on this differing view at the IASB and IFRIC levels (see IASB Staff Paper AP21B — Analysis of expenses by function and by nature, September 2017; and IASB Staff Paper AP21A — Analysis of operating expenses by nature in the notes, April 2022).

The standard-setter eventually took the approach of allowing mixed presentation when issuing the new IFRS 18 Presentation and Disclosure in Financial Statements (at paragraph 78, read together with paragrpahs B80-B85), which will replace IAS 1 for financial years beginning in 2027. That said, IFRS 18 does not create a free choice. An entity must assess which presentation provides the most useful structured summary, considering factors such as the drivers of profitability, internal reporting, industry practice, and whether allocation to functions would be arbitrary.

Frequently asked questions

This information has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax, or other professional advice.

Related articles

library

Essentials of Financial Statements

Financial statements are the primary tools for assessing an entity's fiscal condition. This article covers the key components, how they fit together, and the steps involved in preparing them.

library

Financial Statements Preparation

Financial statements preparation involves converting trial balance data into a complete set of statements compliant with reporting standards. This article covers the process, common challenges, and how automation can reduce preparation time.

library

Lease Accounting Under IFRS 16

IFRS 16 requires lessees to recognise nearly all leases on the balance sheet. This article explains the key concepts, common challenges with inconsistent payment schedules and misaligned lease periods, and how the standard affects financial statement preparation.